Scope 1, Scope 2 and Scope 3 emissions explained

Understanding emission scopes is essential for credible carbon accounting and climate reporting.

Why emission scopes exist in the first place

Emission scopes were introduced to create structure in greenhouse gas accounting. Without a shared way of categorising emissions, organisations risk double counting, inconsistent reporting and unclear responsibility. In practice, emission scopes refers to the three standard categories: Scope 1, Scope 2 and Scope 3 emissions.

The Scope 1, Scope 2 and Scope 3 framework is most commonly defined through the Greenhouse Gas Protocol, which provides widely adopted guidance on how emissions should be categorised and reported.

Emission scopes are one of the core building blocks of carbon accounting. For a broader explanation of carbon accounting as a data discipline, see What is carbon accounting — and why it matters for decision-making.

Scopes do not define ownership of emissions in a legal sense. Instead, they define how emissions are grouped and attributed within carbon accounting — based on operational control, purchasing decisions and value-chain relationships.

Key

Takeaways

- Emission scopes define responsibility, not ownership

- Scopes reduce double counting and reporting ambiguity

- Clear scope logic improves data quality and comparability over time

- Increasing reporting expectations raise the need for consistency

What counts as Scope 1 emissions

Scope 1 emissions are the most direct category. They include greenhouse gas emissions from sources that an organisation owns or controls directly.

In practice, Scope 1 emissions typically arise from on-site activities and company-owned assets, such as:

- Fuel combustion in on-site boilers, furnaces or generators

- Emissions from company-owned vehicles and mobile machinery

- On-site industrial or production processes

- Fugitive emissions, such as refrigerant leakage

- Backup power systems using fossil fuels

For many service-based organisations, Scope 1 emissions are smaller than expected. Even so, they remain strategically important because they are the emissions an organisation has the most direct ability to influence.

What counts as Scope 2 emissions — and where electricity fits

Scope 2 emissions are one of the most common sources of confusion in carbon accounting.

Scope 2 includes indirect emissions from the generation of purchased or acquired energy that the organisation consumes.

This includes:

- Purchased electricity for offices, buildings and facilities

- District heating and district cooling

- Purchased steam or externally supplied heat

Electricity consumption is always reported as Scope 2 — not Scope 3.

Because energy use is central to most organisations, the way electricity-related emissions are calculated has a direct impact on reported Scope 2 results and overall emissions credibility. In particular, the distinction between market-based and location-based Scope 2 is explained in more detail in Market-based vs. location-based Scope 2 emissions explained.

What counts as Scope 3 emissions — and why this scope is different

Scope 3 emissions cover other indirect emissions that occur across an organisation’s value chain. These emissions are not produced by assets the organisation owns or controls, but they are still linked to its activities.

Scope 3 emissions are typically divided into upstream and downstream categories. They reflect the emissions an organisation influences through purchasing decisions, product design and value-chain relationships.

Upstream Scope 3 emissions often include:

- Purchased goods and services

- Capital goods

- Upstream transportation and logistics

- Business travel

- Employee commuting

- Waste generated in operations

Downstream Scope 3 emissions often include:

- Downstream transportation and distribution

- Use of sold products

- End-of-life treatment of sold products

For many organisations, Scope 3 represents the largest share of total emissions — sometimes by a significant margin.

Why Scope 3 emissions are often the hardest to manage

Scope 3 emissions are challenging by nature — not because organisations lack commitment, but because the data often sits outside their direct control.

Common challenges include:

- Dependence on suppliers and value-chain partners

- Limited availability of primary emissions data

- Reliance on estimates, averages and assumptions

For organisations with complex supply chains, Scope 3 calculations frequently rely on industry averages rather than measured data, particularly in early reporting stages.

Do organisations need to report Scope 3 emissions?

Scope 3 reporting is not universally mandatory.

However, sustainability reporting frameworks increasingly expect organisations to assess and disclose material Scope 3 emissions. Within the EU, reporting requirements under the Corporate Sustainability Reporting Directive (CSRD) have significantly increased the focus on reliable and auditable climate-related disclosures.

Organisations are not expected to directly control Scope 3 emissions — but they are increasingly expected to understand, document and explain them.

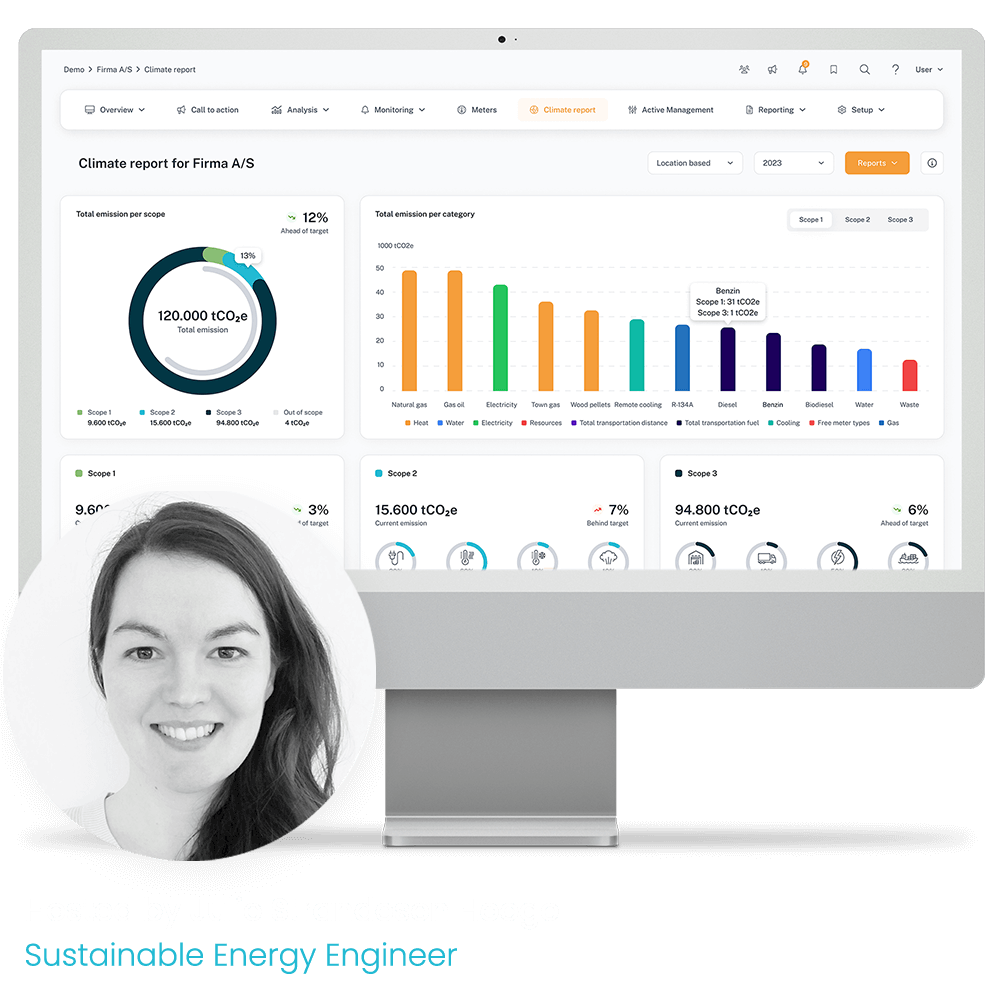

EMS as a practical bridge between energy data and emission scopes

In many organisations, the main challenge in carbon accounting is not understanding emission scopes, but applying them consistently to real-world data over time. Energy and fuel data is often fragmented across sites, meters and suppliers, making it difficult to classify emissions correctly and reproduce calculations year after year.

An Energy Management System (EMS) provides a structured foundation by centralising and validating energy and utility data within a defined organisational model. This allows energy consumption to be consistently linked to assets, sites and activities — which is essential for correctly assigning emissions to Scope 1 and Scope 2.

When carbon accounting functionality is applied on top of this dataset — such as emission factor management and Scope 1, 2 and relevant Scope 3 overviews aligned with the Greenhouse Gas Protocol — emission scopes become a repeatable classification layer.

This reduces reliance on manual interpretation and one-off calculations. This includes support for both market-based and location-based Scope 2 calculations where relevant.

An EMS does not remove the need for boundary definitions or methodological decisions, but it improves traceability by keeping energy data, scope classification, emission factors and reporting outputs connected over time.

Enity EMS is built around this principle, combining structured energy data with transparent scope-based emissions overviews.

Why understanding emission scopes matters for carbon accounting quality

Emission scopes shape how emissions data is collected, how assumptions are applied, and how results can be compared over time.

A repeatable and credible approach typically includes:

- Mapping emission sources

- Classifying them into Scope 1, Scope 2 or Scope 3

- Documenting boundary and classification decisions

- Revisiting scope logic as reporting matures

Conclusion

Scope 1, Scope 2 and Scope 3 emissions provide the structural backbone of carbon accounting.

Clarifying emission scopes early creates a stronger foundation for reporting, supports compliance with evolving requirements, and enables more meaningful and defensible long-term climate strategies.

FAQ about Scope 1, 2 and 3 emissions

What is the difference between Scope 1, Scope 2 and Scope 3 emissions?

The difference lies in where emissions occur and how they are controlled. Scope 1 covers direct emissions, Scope 2 covers purchased energy, and Scope 3 covers upstream and downstream value-chain emissions.

What are Scope 1, Scope 2 and Scope 3 emissions?

Scope 1, Scope 2 and Scope 3 emissions are categories used in carbon accounting to classify greenhouse gas emissions based on direct control, energy purchases and value-chain activities.

What counts as Scope 1 emissions?

Scope 1 emissions include direct emissions from sources an organisation owns or controls, such as fuel combustion in boilers, company vehicles and on-site industrial processes.

What counts as Scope 2 emissions?

Scope 2 emissions include indirect emissions from the generation of purchased electricity, heat, steam or cooling consumed by the organisation.

What counts as Scope 3 emissions?

Scope 3 emissions include other indirect emissions across the value chain, such as purchased goods and services, business travel, transportation, product use and end-of-life treatment.

Is electricity Scope 2 or Scope 3?

Electricity consumption is reported as Scope 2 emissions, not Scope 3.

Do companies need to report Scope 3 emissions?

Reporting requirements vary by jurisdiction, reporting framework, company size, and materiality assessment, but many sustainability frameworks expect organisations to disclose material Scope 3 emissions.

Relevant links & resources on emission scopes

Greenhouse Gas (GHG) Protocol

https://ghgprotocol.org

European Commission

Corporate Sustainability Reporting

ISO 14064

Greenhouse Gas Standards

Webinar On-Demand

How to automate your carbon accounting

An on-demand introduction to carbon accounting — covering core concepts, key legislation, data structure and automation in practice.

- Carbon accounting fundamentals, including Scope 1, 2 and 3

- Key legislation and expectations around sustainability reporting

- How data, emission factors and EMS support consistent carbon accounting

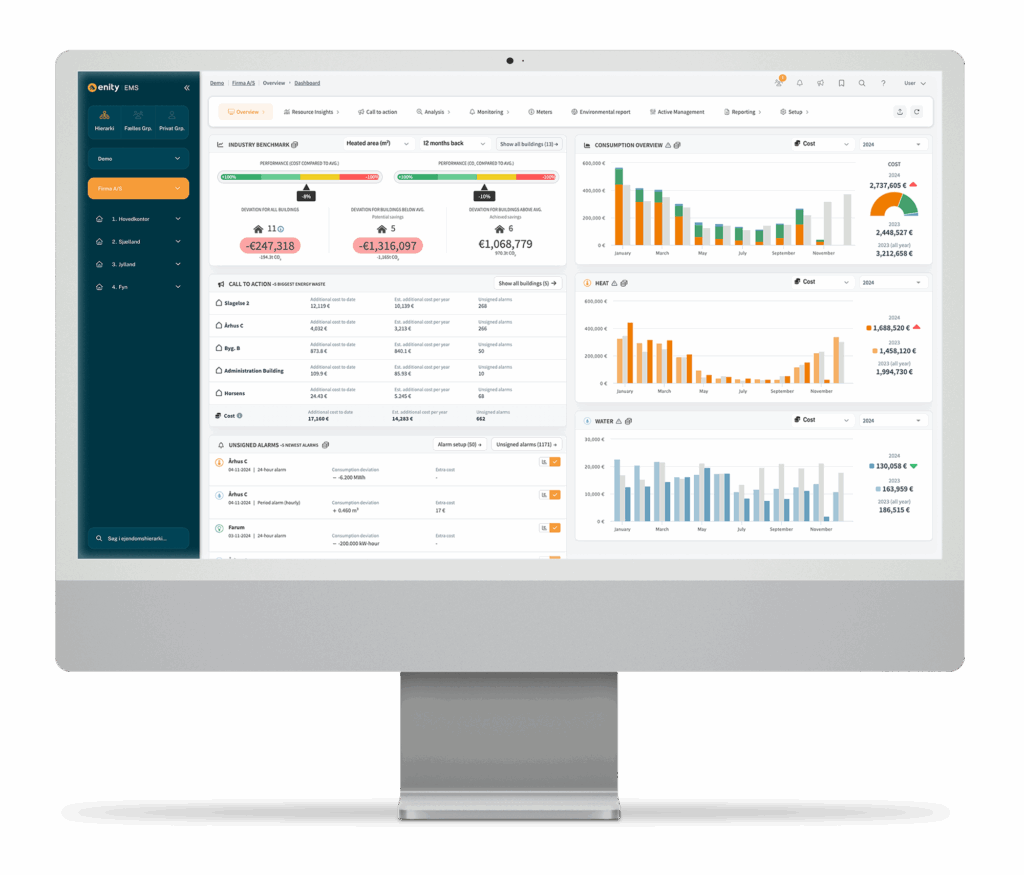

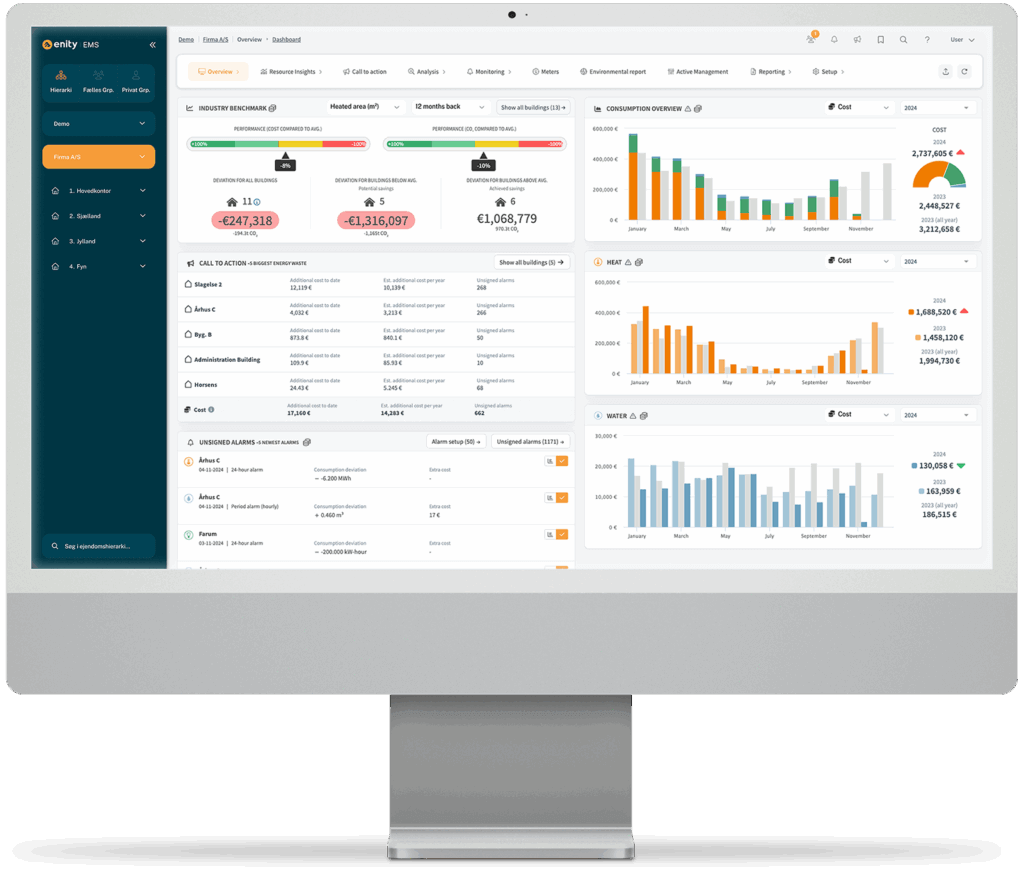

Enity EMS

One platform for all your consumption data

To make confident decisions about your energy consumption, you need insights that are presented clearly, concisely, and in one place. Our goal is to organise your data in a way that means trends are clearly recognised, problems easily spotted, and cost saving opportunities effortlessly identified.

- Dashboards – easy customisation, you decide what you see

- Tracking tools – alerts, budgets, and site comparisons

- Data exports – ready for ESG, CSRD, ISO and internal use

Download brochure

Read more about energy efficiency with Enity EMS. To the benefit of both the budget and the climate.

Book a demo

We show you the possibilities and potentials for optimizing your energy consumption.